Because I work in financial education, people often ask me what I think about the many online tools available to help people manage their money, whether you’re looking to track your budget or your Net Worth. What’s your opinion of mint.com? goes one common query. I don’t have anything against any of these applications per se, but I have to admit that when you ask me, I feel not unlike how I feel at the doctor’s office when the pediatrician asks me how much milk my kids drink—a little defensive and pretty certain I am about to underwhelm you with my answer. I get it, Doc. I live in Wisconsin. Milk for the kids, beer for the adults.

*sigh* I am officially 0 for 2.

So, yes, I understand your expectation that I would not only have an opinion about mint.com or any of its rapidly-proliferating competitors, but could also, in fact, provide you with a succinct assessment of the pros and cons of each and a recommendation for which one might best meet your specific needs and fit your unique personality. Dude, I don’t know how they work and I am too lazy to find out.

See? Underwhelming.

Most of the time when people ask me my take on mint.com or others of its ilk, the question is just that—a simple request for my thoughts. My discomfort with and reluctance to answer the question stems from what I sometimes also hear in the asking—a wistful question behind the question. If I use this one, will I have everything figured out? And my answer to that question, unfortunately, is, No. Technology has truly made our lives better on many fronts, in ways both mundane and breathtaking. Because of these advances, though, we now, too reflexively, expect technology to solve all our problems … and that burden on fintech, as these apps are part and parcel of, is no different.

This is why nobody asks for my opinion about using paper and pencil. You’re not really looking for methodologies. You’re looking for answers.

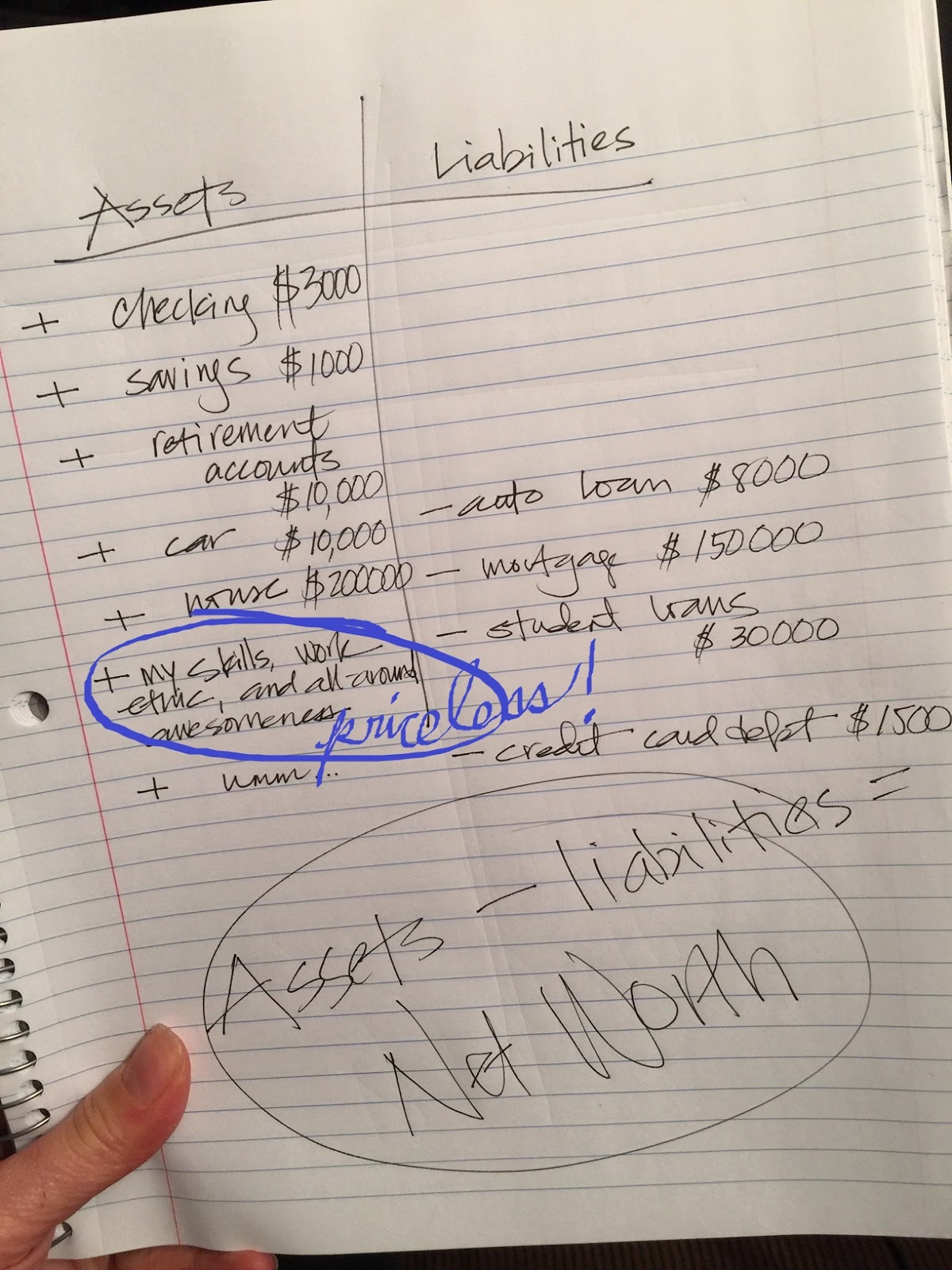

For someone who talks a lot about math and numbers, I don’t actually think that they alone provide a comprehensive or sufficient picture of your financial situation. Let me give you an example. You know how I feel about Net Worth 😀. All that you own minus all that you owe, right?

Not all assets (or liabilities) can be precisely valued. This doesn’t mean they don’t have value. Or that they aren’t an important part of your financial outlook. If anything, they can have more of an impact on your choices than the numbers themselves. When I work with clients, I tell them to add intangible—but real—assets and liabilities to their balance sheet:

Perhaps personal freedom and mobility on one side and the very real likelihood that you’ll have to support a relative on the other. Your ongoing commitment to a charitable cause … asset? Liability?

Does mint.com allow you to do this? Asking for a friend.

If you are in good health with an in-demand skill set and ascetic tastes, your financial situation may be very different from that of someone with a chronic illness working in a declining industry and living in a flood zone, even if you have the exact same Net Worth on paper. Without accounting for all these things, numbers tell me nothing. All those charts that show how much you should’ve saved by age so-and-so? I’m pretty sure they only look at the numbers.

Clearly, Learn more about fintech belongs on the short list for my 2020 New Year’s resolutions. Until then, the best I can answer the question with is, Try it and see how it works for you. How will you know if something, online or off, works for you? Answer a few questions. Do you actually use it? Does it give you a complete picture of your financial situation? Does it help you make decisions? Does it bring you closer to your goals?

Mint.com might check off all the boxes. So might paper and pencil.